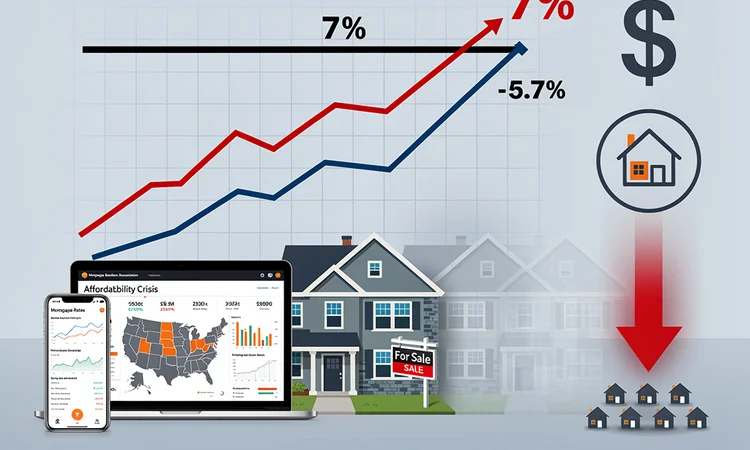

The U.S. housing market’s anticipated spring revival has been abruptly checked by a familiar adversary: rising mortgage rates. A sharp downturn in mortgage demand, the most significant in three months, signals growing fatigue among potential homebuyers confronting a punishing affordability crunch, casting a pall over what is traditionally the busiest selling season.

Total mortgage application volume plummeted 5.7% on a seasonally adjusted basis for the week ending May 24, according to a report from the Mortgage Bankers Association (MBA) . The decline was a direct reaction to a renewed ascent in borrowing costs, with the average contract interest rate for a 30-year fixed-rate mortgage climbing back over a key psychological threshold to 7.05%. This increase effectively erased the brief relief buyers felt earlier in the month and pushed borrowing costs to their highest point in weeks.

A Chilling Effect on Purchase Activity

The chill was most pronounced in the home purchase market, a critical barometer of housing health. The MBA’s Purchase Index, which tracks mortgage applications for home purchases, sank by 1% for the week and was a stark 12% lower than the same week one year ago. This retreat suggests that even motivated buyers are reaching their financial limits as the combination of high prices and elevated rates makes ownership untenable for a growing segment of the population.

“The market is seeing a more notable slowdown in purchase activity, as the recent rise in rates is dampening affordability,” noted Joel Kan, MBA’s Vice President and Deputy Chief Economist. This environment has become particularly difficult for first-time buyers, who lack the home equity of repeat buyers to cushion the blow of higher financing costs. The data underscores a market dynamic where rate fluctuations of even a few basis points can meaningfully alter buyer behavior and sideline thousands of potential purchasers.

The Federal Reserve’s Long Shadow

The upward pressure on mortgage rates is inextricably linked to the Federal Reserve’s ongoing battle against inflation and the subsequent reaction in the bond markets. Mortgage rates closely track the yield on the 10-year U.S. Treasury note, which serves as a benchmark for various forms of long-term credit. Recent commentary from Fed officials has reinforced a “higher-for-longer” stance on the federal funds rate, dispelling earlier market hopes for imminent rate cuts.

Investors are now parsing every piece of economic data for clues about the Fed’s next move. While the latest Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, showed a slight cooling in April, it wasn’t enough to signal a decisive victory over inflation, as reported by Bloomberg . This persistent, albeit moderating, inflation keeps bond yields elevated, which in turn translates directly to the higher mortgage rates confronting consumers at the lender’s office.

Refinancing Remains in a Deep Freeze

While the purchase market is struggling, the mortgage refinancing sector is nearly dormant. The MBA’s Refinance Index plunged 14% for the week and was 5% lower than the same period last year. This collapse in activity is unsurprising, as the vast majority of current homeowners are locked into mortgage rates secured during the pandemic-era lows, many below 3.5%. With current rates hovering around 7%, there is virtually no financial incentive for these homeowners to refinance.

This “lock-in effect” has broader implications beyond the refinancing business. It contributes significantly to the chronically low inventory of existing homes for sale, as homeowners are reluctant to sell and give up their advantageous mortgage terms. According to the National Association of Realtors , existing-home sales recently slid, in part due to this inventory constraint, which props up prices even as demand softens. The result is a market caught in a stalemate: buyers can’t afford to buy, and sellers can’t afford to move.

The Affordability Squeeze Tightens its Grip

For the average American family, the return of 7% mortgage rates is not an abstract economic indicator but a concrete barrier to homeownership. A rate increase from 6.5% to 7.05% on a $400,000 loan adds approximately $125 to the monthly payment, or $1,500 per year. Over the life of the loan, this seemingly small jump amounts to tens of thousands of dollars in additional interest payments, a daunting prospect for households already squeezed by inflation in other areas.

This persistent affordability crisis is reshaping the very structure of housing demand. According to a CNBC analysis of the MBA data, demand for adjustable-rate mortgages (ARMs) has ticked up slightly as some buyers seek lower initial payments. However, this is a niche solution and carries its own risks. The larger trend is one of buyer withdrawal, with many either postponing their search indefinitely or being priced out of their desired neighborhoods entirely.

A Stalled Market Heading into Summer

The latest drop in mortgage applications represents a significant setback for the real estate sector. Lenders, real estate agents, and homebuilders were all banking on pent-up demand to fuel a more robust spring season. Instead, they are facing a hesitant and financially strained consumer base. As noted by Reuters , the housing market has been a primary victim of the Federal Reserve’s aggressive rate-hiking cycle, and its path forward remains murky.

Industry insiders are now recalibrating their expectations for the summer. Without a substantial and sustained drop in mortgage rates—something that appears unlikely until the Federal Reserve sees conclusive evidence of inflation returning to its 2% target—the housing market is likely to continue its pattern of fits and starts. The dream of a normalized, vibrant market remains deferred, contingent on a macroeconomic environment that is proving stubbornly resistant to change.

Leave a Reply

Your email address will not be published.